What a Goodwill Letter Is

A goodwill letter is a polite written request asking a creditor to remove a negative mark — most often a single late payment — as a gesture of goodwill. You're not disputing that it happened. You're asking them to show some grace because you're otherwise a good customer.

It's different from a dispute. A dispute argues that information is inaccurate or unverifiable. A goodwill letter acknowledges the late payment was real but asks the creditor to remove it anyway. Creditors aren't required to say yes — but many will, especially for one isolated slip on an otherwise clean account.

It costs you nothing but a stamp and a few minutes, which makes it one of the easiest DIY moves worth trying before anything else.

When a Goodwill Letter Works (and When It Won't)

It works best when the late payment was a one-time mistake, you have a solid history with the creditor, the account is now current or paid off, and there was a genuine reason — a medical issue, a job change, an autopay glitch.

It rarely works on a pattern of late payments, on accounts already sold to a third-party collector, or when the creditor has a strict no-adjustment policy. Collection agencies in particular tend to be far less receptive than the original creditor.

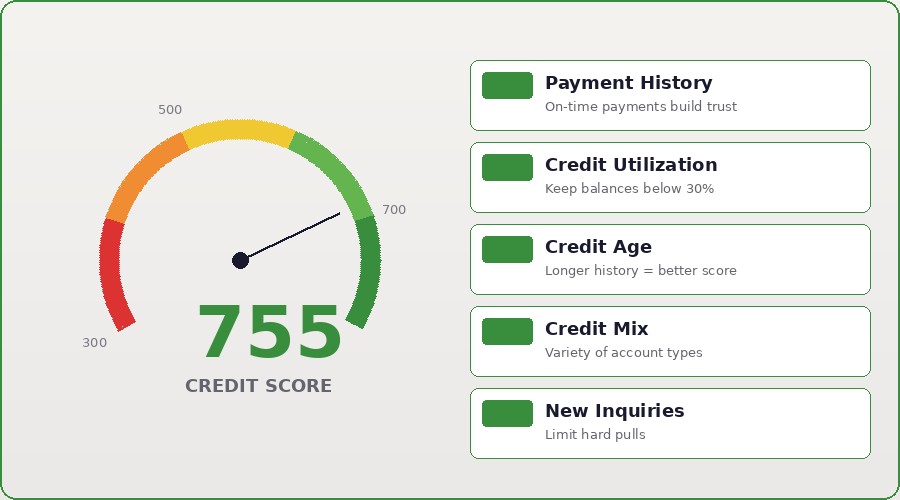

Manage your expectations: a goodwill letter is a request, not a right. A 'no' costs you nothing and a 'yes' can lift your score noticeably, since payment history is 35% of your FICO score.

How to Write One That Gets Read

Keep it short, warm, and specific. Open by thanking them for the relationship and naming how long you've been a customer.

Take responsibility — don't make excuses. Briefly explain what happened, then point to your track record before and since.

Make a clear, single ask: that they remove the late-payment notation from your credit reports with all three bureaus as a goodwill adjustment.

Include your account number, the date of the late payment, and your contact information. Send it to the creditor's executive or customer-service correspondence address, not the payment remittance address.

A Sample Goodwill Letter Template

Dear [Creditor Name] Customer Care Team,

I'm writing about my account ending in [last 4 digits]. I've been a customer since [year] and value our relationship. On [date], a payment on this account was reported [number] days late.

I take full responsibility. At the time, [brief, honest reason — e.g., a family medical emergency / a banking error that disrupted my autopay]. Aside from that single lapse, I have consistently paid on time, and the account is now [current / paid in full].

I'm respectfully requesting a goodwill adjustment to remove this late-payment notation from my credit reports with Equifax, Experian, and TransUnion. It would genuinely help as I work toward [a mortgage / lowering my rates / rebuilding my credit].

Thank you for considering my request. Sincerely, [Your Name], [Account Number], [Phone], [Address].

What to Do If They Say No

Don't take the first no as final. A different representative, or the same letter sent again a month later, sometimes lands differently. Polite persistence pays off.

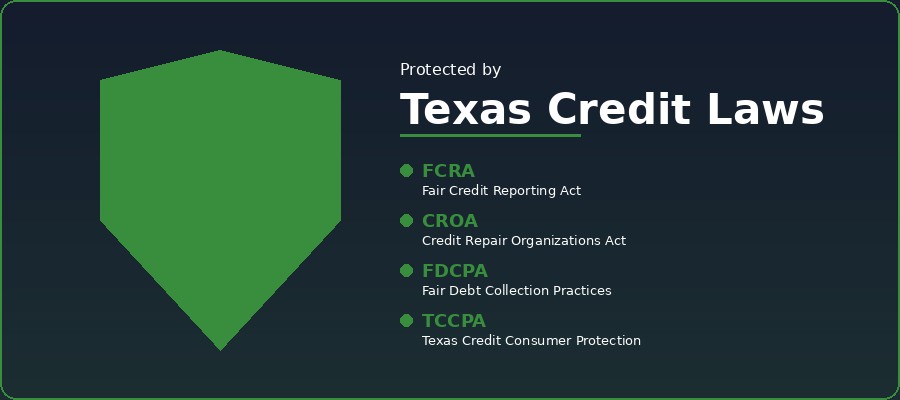

If the late payment is actually inaccurate — wrong date, wrong amount, or it wasn't really late — that's no longer a goodwill matter. You have the right to dispute it under the Fair Credit Reporting Act, and the bureau must investigate.

If the account has gone to collections, your strategy shifts toward your rights under the FDCPA and the dispute process rather than goodwill.

Let 755CreditScore Handle the Heavy Lifting

Goodwill letters are a great DIY first step, and we encourage clients to try them. But when there are multiple marks, accounts in collections, or disputes that need to be done right, doing it yourself can get overwhelming fast.

We know which approach fits which situation — goodwill, dispute, or escalation — and we've used all of them to help over 4,500 Houston-area clients clean up their reports under the protections federal law provides.

Start with a free consultation. We'll review your report and tell you exactly which late payments are worth a goodwill letter and which call for a different play.