If you want to know how to improve credit, the most useful thing to understand first is what actually drives the number. A FICO score isn't a mystery — it's built from five weighted inputs, and once you know which ones move fastest, you can stop guessing and start making changes that show up on your next report. This guide walks through all five, the order to tackle them in, and a realistic timeline for results. If your credit has real damage to undo, also see our step-by-step guide on how to fix your credit score.

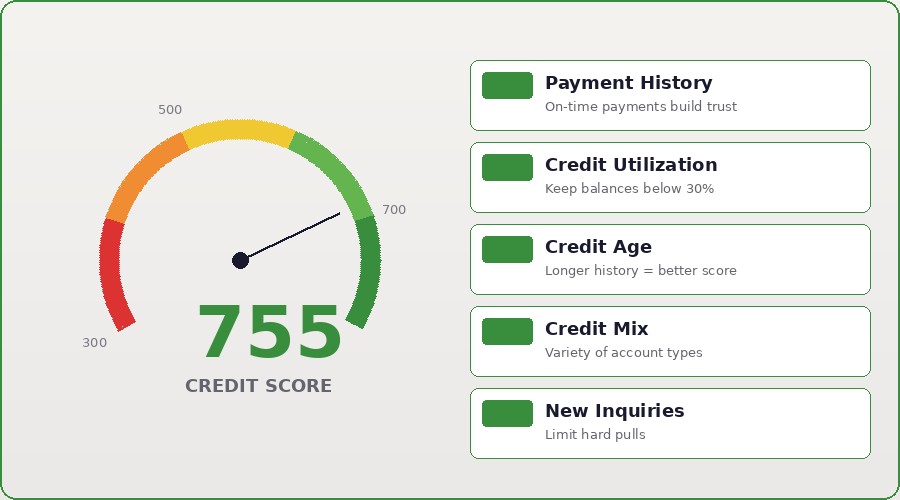

Here's how the five factors are weighted:

- Payment history — 35% (the biggest factor)

- Credit utilization — 30% (the fastest to move)

- Length of credit history — 15%

- Credit mix — 10%

- New credit and inquiries — 10%

1. Lower your credit utilization (the fastest win)

Utilization is the percentage of your available revolving credit that you're using, and at 30% of your score it's the single fastest lever you can pull. If you carry $4,000 across cards with a $5,000 total limit — that's 80% — paying it down to $1,000 (20%) can lift your score 30 to 50 points within one statement cycle.

The trick most people miss: pay before the statement closes, not just before the due date. The bureaus see whatever balance is reported on your statement closing date, which is usually three to four weeks before your payment is due. Pay early and the reported balance is low; pay only by the due date and a high balance may already have been reported. Aim for under 30% as a floor and under 10% if you can. Per-card utilization matters too, so knock down any single maxed-out card first. Our deep dive on credit utilization and the 30% rule covers the timing tactics in detail.

2. Protect and rebuild your payment history

Payment history is 35% of your score — the biggest factor — and it's also the slowest to repair, which is why protecting it comes first. You can't undo a late payment from last year, but you can stop adding new ones. Put every account on autopay for at least the minimum so a single forgotten bill can't cost you 100 points. Better yet, schedule payments a few days early to build a buffer against processing or banking delays.

If you've already fallen behind, getting current is the top priority — the longer an account sits past due, the more it hurts. If a late payment was a one-time slip, a goodwill or procedural dispute can sometimes get it removed. And if you're rebuilding from serious damage, a secured credit card gives you a fresh account that reports perfect on-time history every month.

3. Pay down debt in the right order

How you pay down debt matters for your score, not just your interest. Prioritize credit card balances first, because they directly lower utilization and produce the quickest score impact. Auto loans and mortgages matter less here, since their balances decline naturally over time.

Two cautions. First, don't close a card after you pay it off — closing it shrinks your available credit and can actually raise your utilization overnight. Leave it open and use it occasionally. Second, be careful with old collections: paying one can reset its "date of last activity" and make it look newer and more damaging. For collections and charge-offs, negotiating removal (pay-for-delete) is usually smarter than simply paying an old balance. If you're not sure which accounts to touch, that's exactly what a free credit review is for.

4. Build a healthy credit mix and length of history

Credit mix (10%) rewards you for managing different types of credit responsibly. If you only have credit cards, adding one installment loan — an auto loan, a personal loan, or a credit-builder loan from a credit union — can help your mix. Length of history (15%) rewards older accounts, so keep your oldest cards open and active.

One of the fastest ways to add age and positive history is to become an authorized user on a parent's or spouse's older card that's in good standing. The account's history can feed into your report within 30 to 60 days, and accounts with five or more years of perfect history have the most impact.

5. Remove inaccurate negative items

Nothing drags a score down like collections, charge-offs, and reporting errors — and a surprising number of them are inaccurate or unverifiable. Under the Fair Credit Reporting Act (FCRA), you have the right to dispute any item that's wrong, and the bureaus must investigate. Start with items that have clear errors: wrong dates, wrong balances, or accounts that aren't yours. Those have the highest removal rates.

This is where professional help pays off. Juggling multiple disputes, knowing which items to challenge, and handling reinsertions takes strategy. Our team handles collections removal, charge-off disputes, and full credit restoration under the protections of the FCRA and FDCPA.

6. Be smart about new credit and inquiries

New credit is 10% of your score. Each application creates a hard inquiry that can shave off a few points, so only apply when the benefit is real. If you're rate-shopping for a mortgage or auto loan, do all of it within a 14-day window so FICO bundles the inquiries into one. Avoid opening several new accounts at once, which can signal risk to lenders.

7. Monitor your score so you know what's working

You can't improve what you don't measure. Free monitoring through your card issuer or a service like Credit Karma lets you watch the effect of each change and catch new problems early. Check your full report from all three bureaus — Equifax, Experian, and TransUnion — since an error on one can hold you back even if the others look fine. You can start by learning to check your score for free.

8. Consider getting professional guidance

Many of these steps you can do yourself. But if you have multiple negative items, accounts in collections, the aftermath of identity theft, or you simply want it handled correctly the first time, a credit correction company can accelerate things. At 755CreditScore we've spent more than ten years helping over 4,500 Houston-area clients improve their credit the right way — by using the rights you already have under federal law. Learn more about credit repair in Texas or how our services work.

9. A realistic timeline for improving your credit

Patience matters, but you'll see movement sooner than most people expect:

- Weeks 1–4: Lower utilization and set up autopay. The first score movement often appears here.

- Months 1–3: Utilization reductions and authorized-user history start showing results. Scores usually climb noticeably.

- Months 3–6: Dispute resolutions come through and improvements compound. This is where most clients see real gains.

- Months 6–12: Negative items age, positive history grows, and significant improvement sets in.

- Year 1+: Old negatives fade and steady habits lock in lasting credit health.

Frequently asked questions about improving credit

How can I improve my credit score fast?

The fastest way is to lower your credit utilization. Pay revolving balances below 30% (ideally under 10%) before your statement closing date, and your score can jump 30 to 50 points within one billing cycle.

What hurts your credit score the most?

Payment history at 35% — so late payments do the most damage — followed closely by high credit utilization at 30%.

How long does it take to improve your credit score?

Most people see meaningful improvement in three to six months. Utilization changes can show within one statement cycle; disputes and new positive history take longer.

Does checking my own credit lower my score?

No. Checking your own credit is a soft inquiry and never affects your score. Only hard inquiries from applying for credit can, and only by a few points.

Can I improve my credit on my own?

Often, yes — for utilization and on-time payments. For multiple negatives, collections, charge-offs, or identity theft, professional help under the FCRA and FDCPA usually moves faster.